As the first half of 2019 comes to close, so does PLM’s Relationship Enhancement Program (REP). This program was rolled out in early January 2019 to address a number of growing loss trends specific to the lumber, woodworking and forest products industry. Our commitment to loss control is part of our history and our future. For 125 years we’ve been dedicated to helping our insureds prevent or reduce the losses associated with fires in the wood niche. Yet as the U.S. economy continues to expand and your businesses evolve to meet the demand, businesses take on new product lines, deliver more material, hire additional drivers, and install or subcontract installation of products. These opportunities signify new risk exposures, which present both opportunity and potential liabilities that need to be considered.

REP in Review

PLM has long been known for having personal relationships with our insureds, a hallmark of what makes us different than other insurance companies. In 2019, building and re-establishing relationships was a primary objective along with providing consultative loss control services to improve the overall quality and safety of the business we insure. We freed up the PLM Business Development Team and Loss Control Staff to engage our customer base, setting out on a six-month program to visit more than 9,000 insured locations. That represents approximately 70 percent of our entire book of business.

We selected these 9,000 locations based on a set of criteria that would provide us with the greatest return on our efforts. We identified accounts and/or locations that we haven’t visited in the past 12 to 24 months. Also, we looked at accounts with 20 or more power units to assist them in setting up a formal fleet safety program and a continuous MVR monitoring program (for which PLM pays the administration cost to setup). Primary manufacturing (sawmills and pallet operations) were also on the list to visit to ensure they followed our loss control standards, including a documented hot works program. We want our insureds to remain in business by taking the necessary steps required to minimize the losses associated with operating in the lumber, woodworking and forest products industry.

For the 9,000 locations surveyed, we made more than 7,000 Recommendations for Improvement on approximately 3,000 accounts. When you visit as many locations as we did you’re bound to come across some surprises. We identified 71 locations that were recommended for cancellation for a number of reasons. The most common reasons were that a location was deemed to be in disrepair, vacant, or outside our underwriting appetite.

In addition, a number of accounts were cancelled due to non-compliance of recommendations, which leads me to an important issue:

Recommendations for Improvement. Our loss control recommendations are intended to be a value-added benefit of your policy premium. We want to help raise the safety culture of every insured by acting in a consultative manner to help improve your business.

Unfortunately, sometimes loss control recommendations are not viewed as a positive but rather an annoyance. For instance, if we recommend improved housekeeping around a table saw and the owner reluctantly complies with the recommendation by having the area cleaned up, we have not met our objective. We’re looking to affect the root cause of the recommendations, and that starts and ends with management’s attitude. If management does not believe cleaning up around the table saw every day is important, then what have we accomplished?

Loss control trends

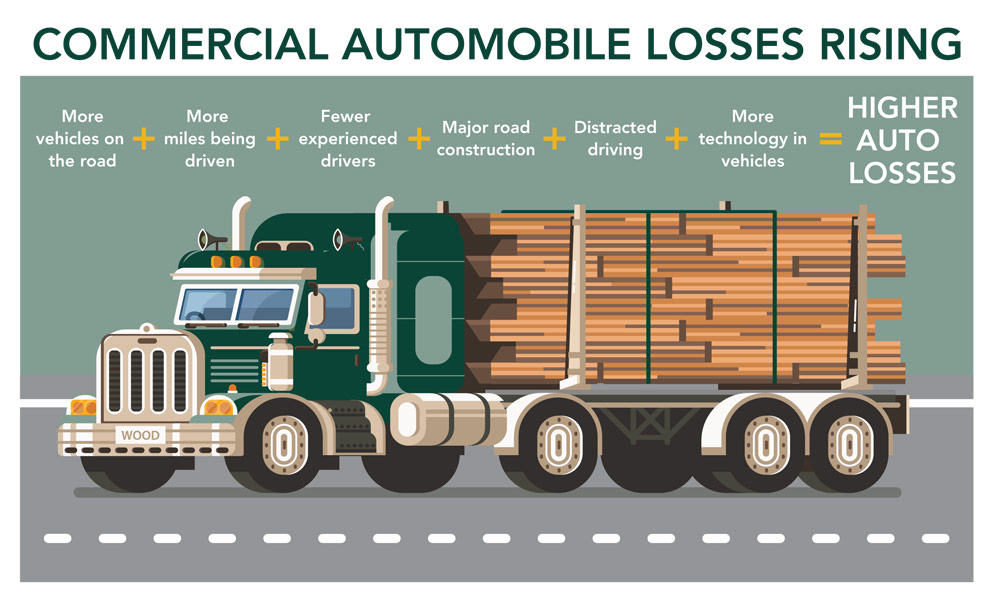

Industry loss trends leading up to 2019 point directly at increased activity in the area of casualty-related losses stemming from new and increased exposures. Whether you’ve recently picked up a newspaper or get your news from the internet, you’ve probably read about the ongoing problems associated with the commercial automobile insurance marketplace. Simply stated, there are more vehicles on the road, more miles being driven, a lack of experienced drivers, major road construction, distracted driving, and more technology in vehicles. These are just a few reasons why automobile losses continue to climb across the country and in the lumber and woodworking industry.

Rising automobile losses necessitate a documented fleet safety program that provides drivers with clear expectations and consequences. Continuous MVR monitoring and the installation of dash cams are another great way to effectively manage the behavior of your drivers.

Current loss trends continue to point towards two other areas of concern. Loading and unloading losses continue to climb. Often, drivers want to be near their vehicles while being unloaded. Forklift traffic and shifting loads present a real danger to drivers. To protect drivers, drivers need to have a designated safety area or remain in the cab.

Current loss trends continue to point towards two other areas of concern. Loading and unloading losses continue to climb. Often, drivers want to be near their vehicles while being unloaded. Forklift traffic and shifting loads present a real danger to drivers. To protect drivers, drivers need to have a designated safety area or remain in the cab.

Furthermore, we have seen losses related to contractors performing work on the behalf of an insured. This has occurred as businesses have evolved by taking on new operations such as installed sales or rental operations. Contractual risk transfers, hold harmless agreements and additional insured certificates need to be carefully managed. Contractors performing work on your behalf, whether on a jobsite or at your premises need to provide evidence of insurance, name you as an additional insured on their policy, and with policy limits that are adequate for the work they’re performing.

As we wrap up our Relationship Enhancement Program at PLM and move into the second half of 2019, we need to continue to refine and improve the programs we have in place. Managing risk is more important than ever and businesses need to be proactive to address these exposures before they become a problem. The safety culture of an organization starts at the top and having an insurance partner that supports your efforts is critical to the success of your safety programs. Let us know how we can assist your business in becoming a safer and, ultimately, a more profitable business.